TAKE NOTE (Insights and Emerging Technology)

Barely one year ago, the world of security clearances was in crisis. The backlog of investigations for individuals seeking a clearance was well over 700,000 — an all-time high. This backlog created a shortage of cleared workers, with critical government functions delayed or deferred.

Recent actions have dramatically reduced the investigations backlog, now below 350,000 and approaching a steady-state number. However, increases in the number of completed investigations created a new backlog in the next step of the process, which is the adjudication decision of whether to grant a clearance to individual government workers, military personnel, or contractors. Despite this new backlog and the continued long wait times, the security clearance process has made progress.

![]()

Big changes are underway. On Oct. 1, the Department of Defense takes over the background investigation mission for the entire federal government, adding it to a new Defense Counterintelligence and Security Agency, or DCSA. DoD is implementing a Continuous Evaluation program. CE is designed to catch problems as they emerge, rather than when a cleared individual is periodically reviewed. In addition, a major executive branch initiative is underway, entitled “Trusted Workforce 2.0.” Together, these improvements will help counter increasing threats from both external and internal sources.

The federal contracting industry has a huge stake in the success of these initiatives. Private sector firms who work on government contracts are committed to the missions of their customers. To meet that commitment, they provide flexible and a responsive workforce with clearances. When those clearances are delayed, that workforce cannot respond as effectively. Important work remains unattended, and companies can fall short of contract requirements and even lose revenue.

Interested in learning more about RPA? Download our FREE White Paper on “Embracing the Future of Work”

UNDER DEVELOPMENT (Insights for Developers)

Blockchain Explained

You’ve probably heard that the blockchain is a technology that is going to change the world — it is the backbone of Bitcoin, the now infamous cryptocurrency. You might even have heard someone trying to explain blockchain by describing it as a “trusted distributed ledger.”

If you’re like most people, that’s when you stopped understanding — or even trying to understand — what this whole blockchain thing is all about. if you have 30 minutes, give this a read and I will do my best to explain it as I understand it and how Governments are using it today.

An Overview of Blockchain

Blockchain was introduced to the world as the record-keeping mechanism for the cryptocurrency Bitcoin which was designed as an alternative to the global financial system and fiat money backed by central governments. Bitcoin wasn’t the first digital currency experiment, but it was the first to solve the problem of securing scarce digital assets. Blockchain is a database distributed over thousands of computers that maintains the list of transactions (called blocks) for each Bitcoin. This prevents users from spending the same Bitcoin multiple times. This established a sense of trust between buyers and sellers, often half a world away, without the need for a central broker.

In 2017, the G20 issued a statement encouraging countries to explore blockchain as an option for strengthening economic resilience and restoring faith in global trade. The statement recognized blockchain technologies as an opportunity to replace regulatory hurdles, but also notes that there are risks including tax evasion, money laundering, and terrorist funding. Blockchain’s ability to transparently record and verify transactions can improve government oversight. The statement includes a proposal for the “the establishment of a global regulatory sandbox for the most promising blockchain use cases” that would support startups and multicultural projects. The IMF, World Bank, OECD, and World Economic Forum are also looking the potential applications and risks of blockchain technologies.

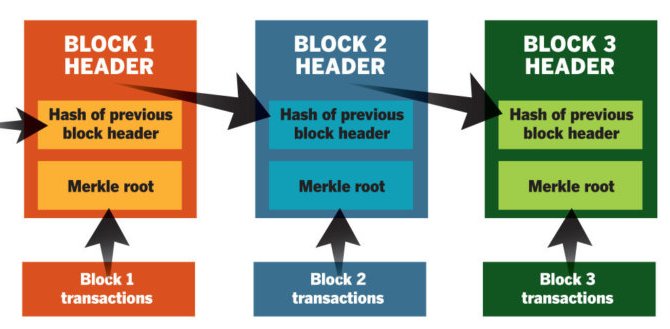

What is Blockchain

Defining blockchain as a new type of database can be misleading. Blockchain extends the capabilities of a traditional database. The transactions in a conventional database often require a third-party to establish trust. For example, when you make a purchase with a credit card, the bank that supports that credit card verifies the transaction between you and the merchant. After this verification, the transaction between your credit card account and the merchant’s account is posted in the database. The bank charges a fee to act as the trusted third-party. Blockchain removes the need for a third-party to verify transactions by building security and trust in the architecture. Any changes or updates to the blockchain must be approved by consensus of all the participating parties on the network.

The database for blockchain is decentralized. Any user on the peer-to-peer, distributed network securely completes a transaction with another user without the need of a third-party. The blockchain ledger maintains all the information and cannot be altered after the transaction is complete. It is also transparent. Changing a transaction requires changing the entire database and will be visible to all users on the network. This transparency that allows you to see your transaction and anyone else’s transactions creates trust and keeps the system secure. The transactions are transparent, but the users can stay anonymous without paying a third-party. This combination of anonymity and savings is the main attraction to the businesses and governments.

Dig Deeper – Blockchain

Q&A (Post your questions and get the answers you need)

Q. While this isn’t exactly a SAP question, with the new trend of BlockChain as a Service being thrown around, and the underlying component called a Bitcoin, I was hoping you could explain what a Bitcoin was? How would it be integrated in a SAP ERP system?

A. This is a great question! Bitcoin is a peer-to-peer, digital, decentralized, cryptocurrency.

It is highly innovative and works on the concept of distributed consensus by proof of work concept invented by pseudonymous inventor Satoshi Nakamoto. It is not constrained by any nation’s borders and can be used anywhere in globe unlike traditional fiat currencies. It also does not have any central backing institution and is backed by cryptography and math. Bitcoins may play a very important role in future. Since they are deflationary in nature, the price of bitcoins are supposed to increase over the period of time. Bitcoins are stored in Blocks. A block can be considered as a page in giant public ledger called blockchain.

Making the business case – Innovation, emerging trends, and technologies are at the heart of everything SAP does. Accordingly, blockchain, with its open, global infrastructure upon which other technologies and applications can be built, has been on SAP’s radar for some time now. As part of SAP’s activities to understand and assess emerging trends and technologies, they’re taking a closer look at the blockchain ecosystem and the blockchain technology. They are working with various blockchain implementations and flavors, including Ethereum, MultiChain, and the Bitcoin blockchain.

Reducing the cost and complexity of operations and processes will continue to be a critical focus for companies, and blockchain shows a lot of promise towards reaching this objective. It remains to be seen if solutions based on this technology will truly act as business disruptors and how well blockchain will integrate into existing systems and processes. Done right, SAP believes that, like other types of peer-to-peer interactions, blockchain definitely has the potential to disrupt entire industries.

Cheers!